Market Insights

Mexico Macroeconomic Trends and Real Estate Outlook

July'25

National Macroeconomic News

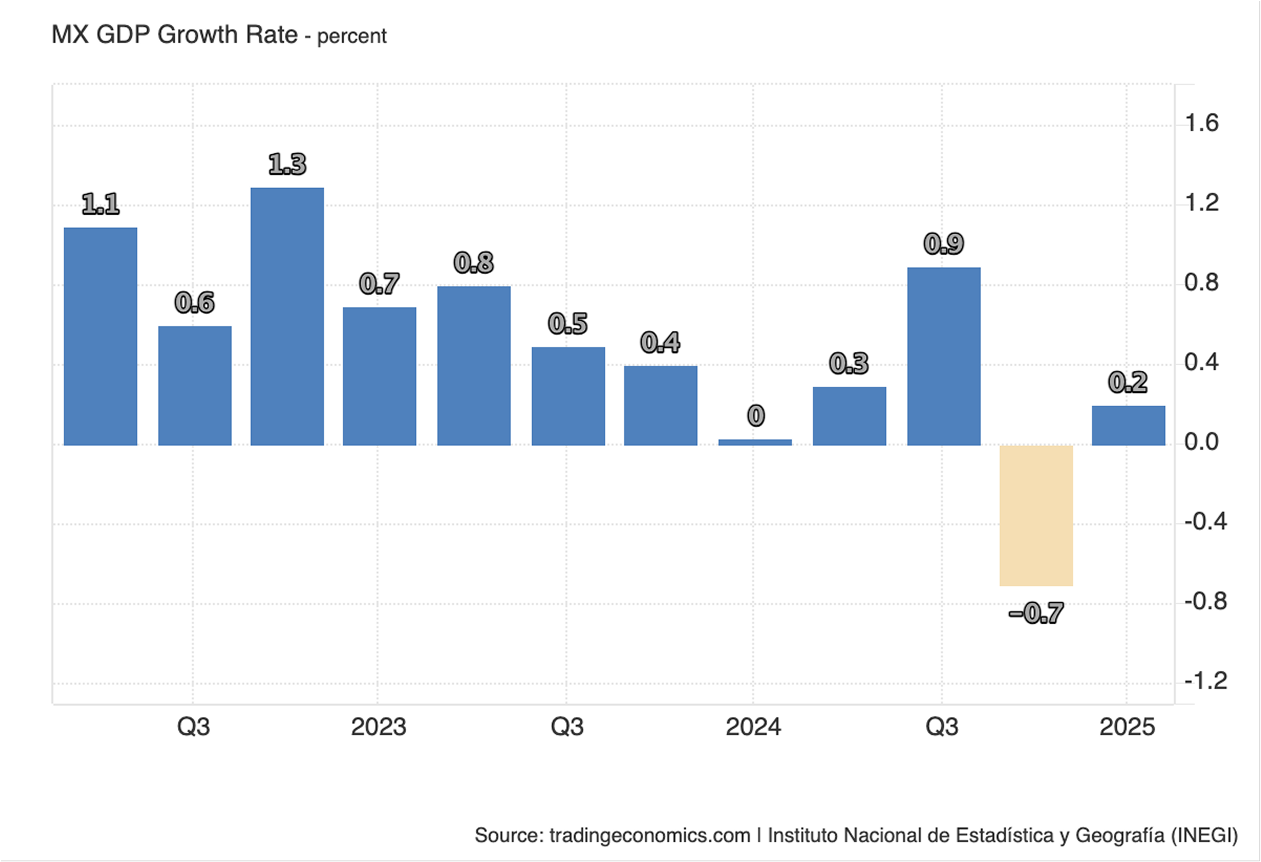

GDP expanded 0.2% quarter-over-quarter in Q1 2025, rebounding from a 0.6% contraction in Q4 which can primarily be attributed to a strong rebound in the agricultural sector with its best quarterly performance since 2011. Uncertainties around trade policy, which have dampened investment and industrial output, caused the industrial and service sector to stagnate.

By skirting recession, macro fundamentals remain intact, and the current growth pause gives investors an entry point before supply tightens in the next upswing.

By skirting recession, macro fundamentals remain intact, and the current growth pause gives investors an entry point before supply tightens in the next upswing.